URBAN TRANSIT AREA REVIEW (2005-1)

Report to/Rapport au :

Transportation Committee / Comité des transports

02 February 2005 / le 02 février 2005

Submitted by / Soumis par : Ned Lathrop, Deputy City Manager / Directeur municipal adjoint

Planning and Growth Management / Urbanisme et Gestion de la croissance

R.T. Leclair, Deputy City Manager / Directrice municipale adjointe

Public Works and Services / Services et travaux publics

Contact Person/Personne ressource : Dennis Jacobs, Director

Planning, Environment and Infrastructure Policy/Politique d'urbanisme, d'environnement et d'infrastructure

(613) 580-2424 x25521, Dennis.Jacobs@ottawa.ca

SUBJECT: | |

|

|

OBJET : |

REPORT RECOMMENDATION

That the Transportation Committee receive this report for information and direct staff to undertake the public consultation process identified in this report and bring forward a report before June 30, 2005 on the results of those consultations and any subsequent recommendations.

RECOMMANDATION DU RAPPORT

Que le Comité des transports prenne connaissance du présent rapport et qu'il donne instruction au personnel de procéder à la consultation publique qui y est prévue et de soumettre d'ici au 30 juin 2005 un rapport sur cette consultation ainsi que les recommandations qui en découlent.

EXECUTIVE SUMMARY

Assumptions and Analysis:

Under the current operational funding approach, transit service is expanded into developed areas that are capable of supporting full transit service. In order to achieve the policy direction provided by Ottawa 20/20 and the 30% transit modal split objective of the Transportation Master Plan (TMP), a more proactive methodology for service expansion should be pursued in order to support transit as early as possible in the early stages of new urban communities.

During the 2004 budget discussions, Council directed staff to develop an appropriate basis and methodology to expand the Urban Transit Area (UTA) and the associated levy in the context of Ottawa 20/20 and the Long-Range Financial Plan. A review of the issue, presented here, indicates that there is no one best methodology for determining how to expand the UTA. There are however, several options that have advantages and disadvantages that should be weighed and discussed by the community prior to staff making a specific recommendation to City Council.

Currently, the UTA defines those areas of the City that receive full transit services and includes those areas that are expected to receive access to full transit services in the short term. The City's UTA boundaries are reviewed annually, as part of the Transplan Report, when new transit services are adopted by City Council. The last revision to the UTA boundary was in 2001, at which time the UTA was expanded to reflect the extension and proposed extension of regular transit service to parts of Ottawa designated as Urban Area in the Official Plan. This included areas that were developing and would be served by transit in the short term, in keeping with the City's historic practice of linking the transit levy to areas capable of supporting full transit service.

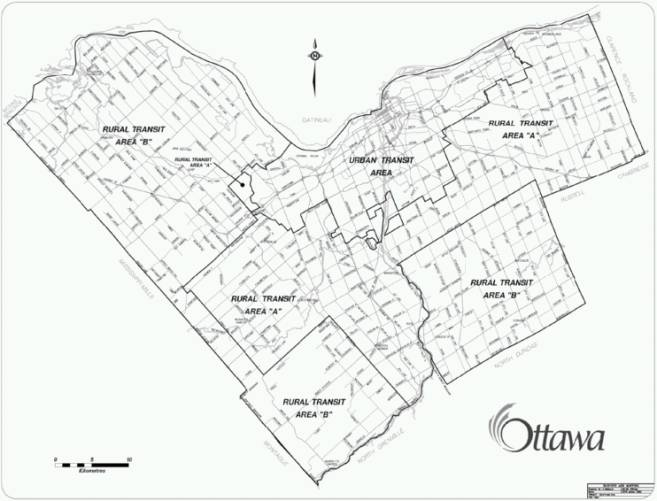

In addition to the UTA, in 2002 City Council approved the establishment of Rural Transit Area A (RTA-A) and Rural Transit Area B (RTA-B), following an extensive consultation process. All three transit areas are shown in MAP 1.

The City of Ottawa's Official Plan and the accompanying Ottawa 20/20 Growth Management Plans recognize the citywide benefits of improved transit for both users and non-users alike. Increasing transit ridership reduces the costs of road infrastructure, reduces congestion on the roads and improves air quality. Both Ottawa 20/20 and the City's Long Range Financial Plan suggest that the net costs of transit should be spread more evenly across the city so that all residents share both the benefits and costs of transit. These objectives were considered when examining the basis for a new approach to expanding the UTA.

The approaches being brought forward for consultation each provide a different balance in apportioning costs between the specific and general beneficiaries of public transit. In particular, this report looks at the following options for funding both the net-operational and net-capital costs of transit, with the intention of bringing these options forward for public consultation.

Options for Net- Operational Transit Funding | Options for Net - Capital Transit Funding: |

A. Maintain the existing approach for expanding the UTA B. Expand the UTA to include all developed urban areas C. Replace the UTA with the Urban Area

| A. Maintain the existing approach for funding the net-capital costs B. Fund the net-capital costs from within the Urban Area

|

It should be noted that both the Official Plan and the Long Range Financial Plan suggest that there is merit in examining the apportionment of net transit costs across the City rather than assigning a specific transit levy to a designated area. This option, although outlined in this report, is not recommended for consideration as part of the consultations at this time, as a 'one size fits all' approach in this instance, could result in a significant financial impact on rural ratepayers currently outside the UTA.

Financial Implications:

This report identifies several options for funding the annual operating costs and net-capital requirements of the transit program, however, the financial implications of the recommended approach will be brought forward in a subsequent report following a full public consultation process.

Public Consultation/Input:

This report will provide the basis of a full public consultation process on this issue. This process will involve four open houses to be held in Cumberland, Stittsville, Barrhaven and downtown Ottawa. The open houses will be advertised in community and citywide newspapers and posted on the City of Ottawa and OC Transpo web sites. The city web pages will also have a copy of this report. In addition, the Pedestrian and Transit Advisory Committee will be consulted.

At the end of this consultation process, staff will bring forward a report, which will include a summary of all comments made by residents and recommended options.

RÉSUMÉ

Hypothèses et analyse :

La méthode actuelle de financement des opérations prévoit l'expansion des services de transport en commun dans les secteurs développés où un service complet se justifie. Pour assurer l'application de l'orientation prévue dans le cadre de l'opération Ottawa 20/20 et faire en sorte que le transport en commun représente 30 p. 100 des déplacements, comme le prévoit le Plan directeur des transports, il conviendrait d'opter pour un mode d'expansion plus proactif qui favorise l'implantation du service de transport en commun dès les tout premiers stades de l'aménagement des nouvelles collectivités urbaines.

Au cours des discussions sur le budget de 2004, le Conseil a enjoint le personnel d'élaborer des critères et une méthode appropriés pour l'expansion du secteur de transport urbain et l'instauration de la cotisation connexe, dans le contexte d'Ottawa 20/20 et dans le respect du Plan financier à long terme. Or, l'examen de la question présenté ici montre qu'il n'existe pas de méthode optimale pour déterminer le mode d'expansion du secteur de transport urbain. Il existe toutefois plusieurs options, qui comportent chacune des avantages et des inconvénients, dont la collectivité doit tenir compte et discuter avant que le personnel ne puisse formuler une recommandation précise au Conseil municipal.

À l'heure actuelle, le secteur de transport urbain comprend les parties de la ville qui bénéficient d'un service de transport en commun complet ainsi que les secteurs qui seraient censés bénéficier d'un tel service à brève échéance. Les limites du secteur de transport urbain sont examinées chaque année, au moment de la production du rapport TRANSPLAN, à la suite duquel le Conseil municipal établit de nouveaux services de transport en commun. La dernière révision des limites du secteur de transport urbain remonte à 2001. Celui-ci a alors été étendu pour tenir compte de l'extension effective ou projetée du service régulier de transport en commun aux parties de la ville désignées comme région urbaine dans le Plan officiel. Il s'agissait notamment de secteurs en développement qui devaient être desservis par le réseau de transport en commun à court terme, conformément à la pratique établie à la Ville, qui consiste à percevoir la cotisation au transport en commun dans les secteurs ou un service complet est justifié.

D'autre part, le Conseil municipal a approuvé en 2002, au terme de vastes consultations, l'établissement du secteur de transport en commun rural A (Secteur rural A) et du secteur de transport en commun rural B (Secteur rural B). Les trois secteurs de transport en commun sont illustrés sur la CARTE 1.

Le Plan officiel de la Ville d'Ottawa ainsi que les plans de gestion de la croissance Ottawa 20/20 reconnaissent que l'amélioration du transport en commun procure des avantages aux usagers comme aux non-usagers et ce, à la grandeur de la ville. L'accroissement de la fréquentation du transport en commun diminue les coûts d'infrastructure routière, réduit l'encombrement des routes et améliore la qualité de l'air. Tant les plans Ottawa 20/20 que le Plan financier à long terme suggèrent une répartition plus uniforme des coûts nets du transport en commun à l'échelle de la ville, de façon que les avantages et les coûts de ce service soient partagés par tous les résidents. Ces objectifs ont été pris en considération au moment d'examiner les critères d'élaboration d'une nouvelle méthode d'expansion du secteur de transport urbain.

Chacune des méthodes soumises à la consultation prévoit une façon différente de répartir les coûts entre les bénéficiaires particuliers et généraux du transport public. Le présent rapport examine les options suivantes pour le financement des coûts d'exploitation nets et des coûts d'immobilisation nets du transport en commun, en vue de les soumettre à une consultation publique.

Options de financement des coûts d'exploitation nets du transport en commun

A. Maintien de la méthode actuelle d'expansion du secteur de transport urbain.

B. Élargissement du secteur de transport urbain à la totalité des secteurs urbains aménagés.

C. Remplacement du secteur de transport urbain par la région urbaine.

Options de financement des coûts d'immobilisation nets du transport en commun

A. Maintien de la méthode actuelle de financement des coûts d'immobilisation nets.

B. Financement des coûts d'immobilisation nets par la région urbaine.

Il convient de signaler que le Plan officiel comme le Plan financier à long terme affirment qu'il y aurait avantage à envisager de répartir les coûts nets du transport en commun entre la totalité des résidents de la ville au lieu d'imposer une cotisation particulière à un secteur désigné. Bien que cette option soit décrite dans le présent rapport, il n'est pas recommandé de la soumettre à la consultation pour le moment, étant donné qu'elle pourrait avoir d'importantes répercussions financières sur les contribuables ruraux habitant à l'extérieur du secteur de transport urbain.

Répercussions financières :

Le rapport présente plusieurs options de financement des coûts d'exploitation annuels et des coûts d'immobilisation nets du programme de transport en commun. Toutefois, les répercussions financières de la méthode recommandée feront l'objet d'un autre rapport, qui sera produit à la suite d'une consultation publique approfondie.

Consultation publique / commentaires :

Le présent rapport servira de base à une large consultation publique sur ce dossier. Il y aura quatre réunions publiques, à Cumberland, à Stittsville et à Barrhaven, de même qu'au centre-ville d'Ottawa. Ces réunions publiques seront annoncées dans les journaux communautaires et les quotidiens de la ville de même que sur les sites Web de la Ville d'Ottawa et d'OC Transpo. Le rapport sera également affiché sur le site Web de la Ville. Le Comité consultatif sur les piétons et le transport en commun sera consulté.

Au terme de la consultation publique, le personnel soumettra un rapport qui résumera les commentaires formulés par les résidents et précisera les options recommandées.

DISCUSSION

The UTA, RTAs and the transit levy

The property tax transit levy applied within the UTA funds the net-operational costs of transit within the UTA and the property tax levy applied within the two RTAs covers the net operational costs of transit within each of those areas. This amounts to approximately 50% of the regular operational costs of transit and 70% of Para Transpo operational costs within each area. This is consistent with collecting a levy from areas receiving a level of direct service.

As well, the levy in each area covers the net-capital costs of transit not covered by development charges or provincial and federal grants. Consequently, the levy in RTA-B does not include a capital contribution component since only Para Transpo service has been provided there. The RTA-A levy includes an estimated proportionate capital contribution limited to bus purchases, shelters and radio systems (1.5% of 2003 total capital contributions and 1.6% in 2004). All other capital costs have been funded through development charges within the Urban Area, provincial or federal grants and by the levy collected within the UTA.

As a result, the average UTA levy in 2004 to cover both the net-operational and net-capital contributions of transit was approximately $429.19 for a residential property assessed at $247,000 while similar properties in RTA-A and RTA-B paid $69.16 and $9.58, respectively. Transit users in RTA-A and RTA-B pay higher fares ($4.75 for rural express routes) compared to users in the UTA ($3.75 for express routes). Table 1 further details the components of the transit levy.

TABLE 1: Existing (2004) Transit Levy Components ($000)

| ($000) | UTA levy 1 | RTA-A levy 1 | RTA-B levy 1 |

OPERATING: Expenses: Operations: Day-to-day operations including salaries, fuel, vehicle maintenance, etc Fleet depreciation: Gross Operations Less Revenues: Fares 2: Tickets, passes and fare revenue Advertising and Other revenue Direct Operating Fiscal Charges to Transit Fund: Share of indirect corporate costs Fiscal Revenue: Share of payment in lieu of taxes and other corporate revenue Net Tax Requirement for Transit Operations |

191,057

27,630 218,687

(107,720) (2,426) 108,541 37,619

(32,469)

113,691

|

Net-operational contributions: Transitway, light rail, conventional and Para Transpo services, including fleet replacement, within the UTA

112,386 |

Net-operational contributions: Conventional and Para Transpo services, including fleet replacement, within RTA-A

1,149 |

Net-operational contributions: Para Transpo services within RTA-B

156 |

CAPITAL FORMATION: Debt Servicing: Interest on outstanding debt Transit Reserve Fund contributions: Funds contributed from property tax to Transit capital program, excluding fleet replacement.

Tax Requirement for contribution to Transit Capital |

8,281

20,660

28,941

|

Capital contributions

28,411 |

Capital contributions: Contribution for buses, shelters and radio systems supporting rural service 530 |

No capital contributions

0 |

Net Taxation Requirement | 142,632 | 140,797 | 1,679 | 156 |

1 In 2004, the UTA levy was $429.19 for a residential property assessed at $247,000. For similar properties, the levy in RTA-A was $69.16 while the RTA-B levy was $9.58.

2 Fares in RTA-A and RTA-B are $4.75 for Rural Express routes while fares in the UTA are $2.60 for Regular routes and $3.75 for Express routes.

As illustrated in Table 1, the gross cost of the Transit Operating program in 2004 was approximately $219 million, including contributions to fleet replacement. Offsetting gross operating costs are fare revenue and other operating revenue totalling approximately $110 million. Net corporate fiscal costs of an additional $5 million resulted in an operating levy requirement of approximately $114 million.

Annual capital formation costs, including debt servicing and contributions to the Transit Reserve Fund, are also funded by the annual transit levy. In 2004, these costs were approximately $29 million for a total transit levy requirement of approximately $143 million.

The capital formation costs raised from the transit levy are not the only funding source for the capital program. As shown in Table 2, the ten-year capital forecast requires $2.748 billion in transit spending for bus fleet replacement, bus fleet growth, transitway construction and rehabilitation, facility maintenance, light rail, and other transit initiatives. The forecast requirement is funded through anticipated Senior Government contributions of $1.386 billion, development charges of $312 million, anticipated contributions from the Gas Tax Reserve Fund of $67.6 million, debenture debt of $689 million, and Transit Reserve Fund contributions of $292.6 million. It is the Transit Reserve Fund contributions and the debt servicing charges that are applied to the annual transit levy for new transit capital requirements. As per the recommendations of the LRFP, new debt servicing costs will be funded by gas tax revenue, thereby mitigating the incremental increase in debt servicing costs funded from the annual transit levy.

Table 2. 10-Year Transit Capital Forecast (2005 – 2014)

Capital Gross Requirement | Total | % |

Fleet Replacement | 361,166,000 | 13% |

Fleet Growth | 364,450,000 | 13% |

Transitway Growth and Maintenance | 515,728,000 | 19% |

Facilities Maintenance | 49,046,000 | 2% |

Light Rail | 1,432,211,000 | 52% |

Other Transit Requirements | 25,650,000 | 1% |

Total | 2,748,251,000 | 100% |

Capital Funding |

|

|

Senior Level Government | 1,386,633,000 | 50% |

Development Charges | 311,902,800 | 11% |

Gas Tax Reserve Fund | 67,619,000 | 2% |

Debenture Debt | 689,434,000 | 25% |

Transit Reserve Fund | 292,662,200 | 11% |

Total | 2,748,251,000 | 100% |

Concerning the current capital funding approach, all assessed properties in the UTA are the primary source for funding the net-capital costs of transit, including the transitway, light rail, and park and ride facilities. In order to achieve the adequate and equitable transportation funding objectives of Ottawa 20/20, these net-capital costs should be spread more evenly across the city so that all residents share both the benefits and costs of transit. The OC Transpo Comprehensive Review, an extensive report prepared by the KPMG / IBI group and presented to the Transit Services Committee in February 1999, also recommended that transitway and transit-related roadway capital improvements, including park and ride lots, be funded through a citywide process rather than the UTA levy. However, there is a need to also consider the financial impact that any change in the transit levy area will have on those ratepayers outside the area as currently defined.

The OP and the OC Transpo Comprehensive Review support implementing a citywide approach for funding transit based on pursing the goals of transit and to relieve, in the long-term, the pressures on the roadway system. Staff however, recommend that further analysis of the financial implications of this option, are necessary.

Given the policy context provided by Ottawa 20/20 and the recommendations detailed within the LRFP and the OC Transpo Comprehensive Review (Document 3), this report explores the following options for funding both the net-operational and net-capital costs of transit.

Options for Net- Operational Transit Funding | Options for Net - Capital Transit Funding: |

A. Maintain the existing approach for expanding the UTA B. Expand the UTA to include all developed urban areas C. Replace the UTA with the Urban Area

| A. Maintain the existing approach for funding the net-capital costs B. Fund the net-capital costs from within the Urban Area

|

OPTIONS FOR NET-OPERATIONAL TRANSIT FUNDING

Under the current process, the transit levy collected within each designated area covers the net-operational transit costs within each respective area. Integral to this approach is the annual Transplan process, which reviews transit operations and makes recommendations for service changes, which in-turn affects the net-operational costs and the transit area boundaries. Under this current methodology, all parts of the Urban Area that can support full transit service, including parts that are expected to receive full transit service in the short term (i.e. the next 12 months) are added to the UTA on a annual basis.

A. Maintain the existing approach for expanding the UTA

Through maintaining the status quo, a number of existing developments within the Urban Area will continue to be excluded from the UTA even though they receive or have access to transit service.

Properties will continue to be added to the UTA based upon their ability to support full transit service. Consequently, the UTA boundary will continue to expand slowly, as full transit service is extended into newly developed areas. The UTA boundaries will also continue to be reviewed as part of the annual Transplan process, including annual public consultation regarding extensions to services and boundary changes.

The problem with this approach is that development needs to first occur at a level to support full service before transit is expanded. Developed areas that cannot support full service will not be included in the UTA even though extending transit may contribute to further growth and lower transportation costs by reducing the need to plan, build and service new roads. This status quo option also goes against the strategic direction in the Official Plan (OP) of supporting rapid-transit service in the early development stages of new urban communities.

This approach is also inconsistent with the LRFP and the OC Transpo Comprehensive Review as the benefits of transit are viewed in isolation of the overall transportation network.

B. Expand the UTA to include all developed urban areas

Under this approach, all existing developed urban areas would immediately be included in the UTA. Subsequently, the transit area boundaries would expand on an annual basis to include newly developed areas. Public consultation regarding future boundary changes would no longer be required.

This option would involve expanding the current UTA to immediately include about 6,628 additional urban properties (including 5,770 residential properties), located in the communities of Chapman Mills, Gloucester Glen, Heart's Desire, Honey Gables, Morgan's Grant, Notre-Dame-des-Champs, Rideau Glen, Stittsville, Strathearn and the area south of Findlay Creek. As a result, ratepayers in these affected areas would pay higher property taxes (Table 3) without receiving increased service unless operational and capital funding increased or if transit routes were redistributed. Each of these areas would be reviewed to determine their ability to support full transit service and the costs of these services would be brought forward for budget approval through the Transplan process.

Expanding the UTA to include all developed urban areas is compatible with the philosophy that only ratepayers who have access to transit service contribute towards its net-operational costs. However, this approach does not reflect the citywide nature of transit services as many users take advantage of the park and ride facilities to use the service daily but only partially contribute to the cost through their fares. As well, this option does not address the overall benefits for the city achieved by increasing transit usage such as reduced costs for road infrastructure and improved air quality through reduced automobile use.

C. Replace the UTA with the Urban Area

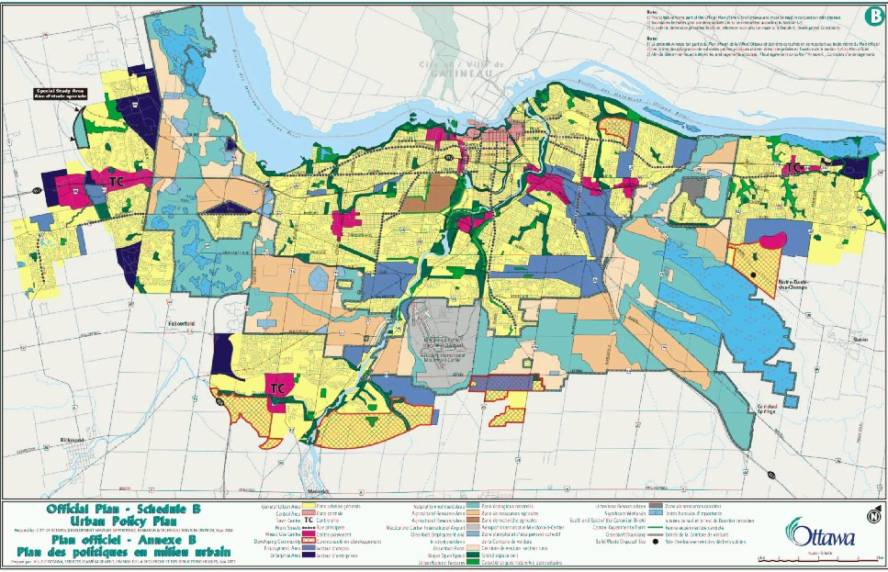

Through replacing the UTA boundary with the Urban Area boundary, defined as Schedule B in the OP (Map 2), approximately 7,718 additional properties (including 6,428 residential properties) would be added to the UTA. The affected properties would include those identified above in Operational Option B, as well as undeveloped properties within the Urban Area boundary. Ratepayers in these affected areas would also pay higher taxes (Table 3) without receiving increased service unless operational and capital funding increased or if transit routes were redistributed. At the outset, each of these areas would be reviewed to determine their ability to support full transit service and the costs of these services would be brought forward for budget approval through the Transplan process.

Under this approach updating and maintaining the UTA as a separate entity would be unnecessary, as it would continue to be defined as the Urban Area in the OP. As well, public consultation with respect to the transit area boundaries would become part of the OP consultation process rather than the annual Transplan process.

This option allows the net-operational costs to be spread evenly over more properties than the current approach or Operational Option B.

D. The implications of spreading the net-operational costs citywide

This approach would see all net-operational transit costs applied evenly across the city, eliminating the need for urban and rural transit areas. Consequently, annual public consultation facilitated through the Transplan process would focus on the extensions of service and no longer include discussions regarding transit area boundaries.

While a single uniform operational levy does not respect the user pay philosophy, it is consistent with the OP and the TMP in that it provides an adequate and equitable approach considering that all city residents benefit either directly or indirectly from transit. Transit users directly benefit from improved service while non-transit users benefit from the alleviation of congested roads and the reduced costs associated with road construction and road maintenance as well as improved air quality. In this context, all residents share the benefits and the costs of transit. However, although this option is compatible with the LRFP and the OC Transpo Comprehensive Review as transit and roads would be funded similarly and would establish an overall citywide transportation solution, rural ratepayers would also pay higher taxes (Table 3) without receiving increased service unless operational and capital funding increased or if transit routes were redistributed. Therefore, this option is not recommended to be brought forward for public consultation.

OPTIONS FOR NET-CAPITAL TRANSIT FUNDING

The net-capital costs of transit are the capital costs not covered by development charges, provincial or federal subsidies. Under the current approach, the majority of the net-capital costs are covered by the UTA levy ($28.41 million in 2004). In addition, the RTA-A levy covers an estimated proportionate net-capital cost ($530,000 in 2004) while the RTA-B levy does not cover any net-capital costs.

A. Maintain the existing approach of funding the net-capital costs

Under the status quo, primarily funding the net-capital costs of transit from the UTA levy, transit users outside the UTA will continue to benefit from the transit system without fully contributing to its capital costs. It has been estimated that approximately 40% of park and ride users live outside the Urban Area, which demonstrates that the current practice is an inequitable approach. This approach is inconsistent with the recommendations put forth by the LRFP to treat transit funding in the same manner as roads. It also does not address the benefits from the alleviation of congested roads and the reduced costs associated with road construction and road maintenance as well as improved air quality.

B. Fund the net-capital costs from within the Urban Area

Under this option, the majority of the net-capital costs of transit would be collected from within the Urban Area, however, RTA-A would also continue to contribute an estimated proportion of capital costs equal to the costs of maintaining transit service within RTA-A.

This approach is also consistent with the way development charges currently fund capital investments in transit. With the approval of the new development charge by-law in June 2004, development within the Urban Area is charged for transit, rather than only within the UTA, as in previous development charge by-laws. While this option would align these two processes, it does not account for park and ride facilities and other transit infrastructure that benefit rural residents. The fact that 40% of park and ride users live outside the Urban Area is even more significant when considering the overall benefits for all residents of an improved transportation system.

C. The implications of spreading the net-capital costs citywide

Although this option is not being recommended to be brought forward at this time, consideration of the implications of this approach will likely be examined at some time in the future, as indicated by the Official Plan and the Long Range Financial Plan. All city residents, both rural and urban, benefit either directly or indirectly from capital investments in transit. Transit users directly benefit from improved service and expanded infrastructure while non-transit users benefit from the alleviation of congested roads, improved air quality through the reduction in personal automobile use and the reduced costs associated with road construction and road maintenance. A single lane of transitway replaces several lanes of road construction which helps to preserve the quality of our natural environment while also minimizing the need to plan, build and service new roads. In view of these benefits, net-capital costs for transit, including those associated with the transitway, light rail, and park and ride facilities, should be shared citywide, similar to the treatment of capital costs related to road projects.

This approach, which would eliminate the need for urban and rural transit areas, is consistent with the policy context of the OP and TMP as it offers a reliable and dependable funding approach that acknowledges transit as a public service that benefits all residents. It also addresses the issue of who pays when transit capital expenditures are increased to offset decreases in road expenditures. Since these benefits are spread across the city, there will be a future review of the potential for distributing the associated net-capital costs in the same manner. This idea will also be examined as part of future updates to the development charge by-law.

RECOMMENDED APPROACH

As noted previously, in order to support the transit objectives of the OP and TMP, the approach to expanding the Urban Transit Area needs to balance the benefits all residents from the alleviation of congested roads, improved air quality and the reduced costs associated with road construction and road maintenance with the direct benefits received by those who have access to public transit service.

Staff are recommending that a modified version of what exists now be pursued, such that both the net-operational costs and the capital contributions are allocated to the Urban Area (Operational Option C and Capital Option B). In this case, taxpayers in the Urban Area who are directly benefiting from service would contribute to the net-operating and net-capital costs of transit. However, staff also recognize that all of Operational Options A, B and C and Capital Options A and B need to be the subject of substantial public consultation prior to a recommendation being brought forward for Committee and Council's consideration.

Subject to the public consultation process outlined in this report, staff will bring forward a recommended approach to the Transportation Committee before June 30th, 2005.

CONSULTATION

This report will provide the basis of a full public consultation process on this issue. This process will involve four open houses to be held in Cumberland, Stittsville, Barrhaven and downtown Ottawa. Transit customers and residents will be invited to these open houses, where they will be encouraged to present their views and provide comments. City staff will be available at the open houses to hear the views of residents and to answer any questions. Residents will also be able to provide their comments and ideas by mail, fax, or e-mail.

The open houses will be advertised in community and citywide newspapers and posted on the City of Ottawa and OC Transpo web sites. The city web pages will also have a copy of this report. In addition, the Pedestrian and Transit Advisory Committee will be consulted.

At the end of this consultation process, staff will bring forward a report, which will include a summary of all comments made by residents and recommended options.

FINANCIAL IMPLICATIONS

This report identifies several options for funding the annual operating costs and net-capital requirements of the transit program. The estimated financial implications for each of these options are listed in Table 3, based on 2004 net-operational and capital requirements.

TABLE 3: Financial Impacts for a Residential Property Assessed at $247,000

UTA 1 | RTA-A 1 | RTA-B 1 | ||||

Operational Levy Amount | Number of residential properties | Operational Levy Amount

| Number of residential properties

(Affected properties) 2 | Operational Levy Amount

| Number of residential properties

(Affected properties) 2 | |

|

|

|

|

|

| |

Option A (Maintain the existing approach for expanding the UTA) | $342.59 | 197, 489 | $47.33 | 17,351 (0) | $9.58 | 13,394 (0) |

Option B (Expand the UTA to include all developed urban areas) | $336.17 | 203,259 | $50.22 | 11,581 (-5,770) | $9.58 | 13,394 (0) |

Option C (Replace the UTA with the Urban Area) | $335.33 | 203,917 | $52.59 | 10,959 (-6,392) | $9.58 | 13,358 (-36) |

The implications of spreading the net-operational costs citywide | $311.47 | 228,234 | $311.47 | 0 (-17,351) | $311.47 | 0 (-13,394) |

CAPITAL |

|

|

|

|

|

|

Option A (Maintain the existing approach of funding the net-capital costs) | $86.60 | 197, 489 | $21.83 | 17,351 (0) | $0 | 13,394 (0) |

Option B (Fund the net-capital costs from within the Urban Area) | $84.94 | 203,917 | $24.28 | 10,959 (-6,392) | $0 | 13,358 (-36) |

The implications of spreading the net-capital costs citywide | $78.52 | 228,234 | $78.52 | 0 (-17,351) | $78.52 | 0 (-13,394) |

1 The UTA, RTA-A, and RTA-B boundaries are defined by each option.

2 Affected properties are defined as properties that become part of the UTA. The remaining properties in each area would be subject to the revised levy amount for their respective area.

SUPPORTING DOCUMENTATION

Document 1 - Map 1: Transit Areas

Document 2 - Map 2: Urban Area

Document 3 - Excerpts from LRFP and OC Transpo Comprehensive Review

DISPOSITION

City Staff will undertake the public consultation phase outlined in this report and prepare recommendations to be submitted for Committee and Council approval.

MAP 1: TRANSIT AREAS Document 1

MAP 2: URBAN AREA Document 2

EXCERPTS FROM LRFP AND OC TRANSPO COMPREHENSIVE REVIEW Document 3

Long-Range Financial Plan 2

October 2004

DOCUMENT 4 - STAFF REPORT SUPPORTING THE RECOMMENDATIONS OF THE LONG RANGE FINANCIAL PLAN COMMITTEE

Funding Strategy

In an effort to confine debt financing to only certain types of projects, the first Long Range Financial Plan contained the following recommendation:

"Long-term debt financing should be restricted to specific project types. Debt funding for lifecycle projects should be reduced and ultimately eliminated. Instead, debt financing should be employed on projects related to capacity expansion or growth, projects financed by development charges, future new non-traditional infrastructure projects, and projects tied to third party matching funding. These restrictions may have to be phased in to meet short-term budget challenges."

The rationale for the use of debt as an effective financing mechanism for the City of Ottawa is that it allows major growth projects to be paid for over a number of years, similar to a mortgage on a home. It spreads the benefit of the capital project over a longer benefit period providing for the project to be paid for by a broader tax base, and it makes the development of required capital works within the 10 year time frame achievable.

In a publication entitled "Mind the Gap, Finding the Money to Upgrade Canada’s Aging Infrastructure" the TD Bank Financial Group in May 2004 addressed the national infrastructure problem and provided a number of proposals. When speaking of the use of debt they said,

"Maintaining low debt-load may be a laudable goal, but if it comes at a cost of foregoing or delaying capital projects because non-debt sources of financing aren't available, then a low-debt strategy is counter-productive." and "Besides, a healthy level of borrowing passes the test of equity, since benefits, which are normally consumed over the life of several decades, are matched with the costs"

The question for the City is how can the use of debt be effectively used without increasing the costs on the property tax bill itself. What staff is recommending is the use of the new non-property tax revenues as a source of funding new debt that could be issued under the existing policy wording. The debt that would be eligible under the definition is predominately associated with the public transit and transportation areas and would be a natural tie into the use of gas tax revenues as a repayment source. It is recommended that debt financing be used to fund the growth portion of the expansion of rapid transit and other growth-related projects by debt financing some projects and using the future stream of gas tax payments to pay the debt charges.

Appendix 1 - Policy Recommendations Contained in the First Long Range Financial Plan

10. The urban or rural transit levy should be earmarked for operating and capital requirements of the transit service (such as buses, garages and other services that directly support the operation) within either the urban or rural areas. As a result, all residents would contribute to future transit extensions in the same manner as they contribute to roads.

Status: The review of the transit levy areas is still pending

City of Ottawa Long-Range Financial Plan: First Steps

October 2002

Funding transportation infrastructure is one of the major challenges of growth. Currently, the City funds transportation initiatives using both the city-wide levy for roads projects and the transit levy for transit initiatives. This funding practice has been carried over from the former Region. The transit levy now provides funding for new and replacement buses, transit maintenance facilities, transitway rehabilitation and expansion and other capital projects identified with the transit operation. Transit capital funding is collected from within the urban transit area only. In the future, expansion of road and transit networks should be funded from the same tax base.

Transportation solutions should be considered on a city-wide basis recognizing that expansion of both the transit and road networks may be required to form the solution. Extension of the transitway or alternate transit services should be seen as a transportation solution in the same manner as road construction and should be funded from the same tax base.

The urban or rural transit levy should be earmarked for operating and capital requirements of the transit service (such as buses, garages and other services that directly support the operation) within either the urban or rural areas. This approach has already been adopted in the rural service strategy.

The City’s capital infrastructure deficit can be reduced by changing the way the City develops. One alternative is investing in high quality transit, which in turn reduces the need to build more arterial roads and expressways. This alternative also provides significant side benefits, such as less air and water pollution, and the creation of high quality community living. Any increase in the share of trips taken by transit reduces infrastructure costs.

OC Transpo Comprehensive Review: The Way Ahead Becoming the Best of the Best

February 1999

Long-Term Strategy

The long-term objectives for OC Transpo support the policies of the Region's Official Plan (OP) and Transportation Master Plan (TMP) to reduce Ottawa-Carleton's dependency on private automobile use and promote more environmentally friendly modes of transportation.

The property tax support of transit is currently limited to properties within the "Urban Transit Area" (the "UTA). This tends to force OC Transpo to serve all areas of the UTA whether transit is the most cost-effective transportation solution or not, and deprives areas such as Stittsville, which is outside the UTA, of appropriate service. It also results in a shift in who pays when transit expenditures are increased to decrease road construction expenditures. This practice should be revised.

Key Recommendations

That OC Transpo focus, in both the short term and the long term, on achieving improved service reliability and attentive customer service, and refrain from providing more service than it can provide reliably.

That Council consider options for reforming the Urban Transit Area (UTA), including:

· phasing out the UTA, with transit funding shifting to the regional levy.

· extending the UTA to include Stittsville.

· including transitway and transit related roadway capital improvements on the regional levy rather the UTA levy.

· including the costs of park and ride lots and related service in the regional levy rather than the UTA levy.